Commentary

When China Says No: What the Reliance-Hithium Episode Reveals About India's Battery Vulnerability

Raghavan S Rao

Jan 17, 2026, 08:19 AM | Updated 08:18 AM IST

In January 2026, Bloomberg reported that Xiamen Hithium Energy Storage Technology Co. had withdrawn from technology-sharing talks with Reliance Industries, citing Beijing's tightening export controls on battery technology. The story suggested that India's largest private company had been denied access to critical cell chemistry know-how, imperilling its gigafactory ambitions.

Both sides swiftly pushed back. Reliance "strongly and categorically" affirmed that its battery manufacturing plans remained on track and that its 2026 timeline was unchanged. Hithium, for its part, stated it had made no comments to the media regarding any partnership discussions.

What neither side denied is equally telling. Reliance did not deny that discussions with Hithium had taken place, nor that such discussions had stalled. Hithium did not deny that technology-sharing arrangements had been explored, nor that Beijing's export controls might constrain future cooperation. The careful, lawyerly responses suggest a story more complicated than either a definitive breakdown or business as usual.

Whether or not a formal technology denial occurred, the episode is instructive. It illuminates a structural vulnerability that India would do well to confront: the country's largest conglomerate, with revenues of $114 billion and a market capitalisation exceeding $220 billion, was reportedly in negotiations to license battery cell technology from a Chinese startup founded in 2019 with revenues of $1.8 billion. Reliance is 63 times larger than Hithium. That such a David-and-Goliath dependency could even be plausible tells you something about the state of Indian industrial capability in critical sectors.

And it raises an uncomfortable question: what happens when China does say no?

The Humiliation Playbook

The question is not hypothetical. Technology denial has been a recurring feature of great-power competition, and its consequences are well documented—nowhere more vividly than in China's own recent history.

Every major Western embargo against China has catalysed the emergence of competitive or superior Chinese alternatives. The pattern is so consistent it resembles a law of industrial development.

Consider BeiDou. In July 1993, the United States jammed GPS signals to the Chinese container ship Yinhe, stranding it at sea for 24 days on false intelligence about chemical weapons. Three years later, during the Taiwan Strait Crisis, Chinese missiles went astray—allegedly because America had again degraded GPS. Chinese state media called these episodes "unforgettable humiliations." Within a year of the Yinhe incident, China had launched the BeiDou programme. Three decades and $10 billion later, BeiDou operates 60 satellites to GPS's 31 and provides superior coverage across Asia, Africa, and Latin America. A 2022 American government advisory board admitted, with evident discomfort, that GPS is now "substantially inferior" to its Chinese rival.

The semiconductor story is more recent and still unfolding. When Washington added Huawei to the Entity List in 2019 and blocked ASML's extreme ultraviolet lithography machines, experts predicted China would fall permanently behind. Instead, in August 2023, Huawei launched a smartphone powered by a 7nm chip manufactured entirely in China—without EUV equipment—during the visit of America's Commerce Secretary. China has since committed over $100 billion through its "Big Fund" for chip self-sufficiency.

The pattern holds across domains. The Wolf Amendment of 2011 banned NASA from cooperating with China; by 2022, China had its own permanently crewed space station. The post-Tiananmen arms embargo cut off Western military technology; today China fields the J-20 stealth fighter and Type 055 destroyer, both developed entirely under sanctions. In 2015, America banned Intel and Nvidia from supplying supercomputer chips; within 14 months, China unveiled the world's fastest supercomputer running on indigenous processors.

The lesson is not that technology denial is painless. Initial gaps are real, quality suffers, and timelines stretch across decades. But the strategic outcome is consistently transformation: from vulnerability to capability, from dependence to independence, and often from student to competitor.

The Vulnerability the Episode Exposed

Return, then, to the Reliance-Hithium affair. Even if no formal denial occurred, the mere plausibility of such a scenario exposes India's structural dependence on Chinese battery technology—a dependence that Beijing could exploit at any moment through its expanding export control regime.

China tightened restrictions on lithium battery technology transfers in October 2025. The controls require export permits for strategic technologies and give Beijing broad discretion over what crosses its borders. A company like Hithium, however willing it might be to partner with Indian firms, operates within a regulatory environment that could foreclose such cooperation at any time. The decision may not rest with the company at all.

This is the crux of the matter. India's battery ambitions—central to its electric vehicle transition and its net-zero commitments by 2070—currently depend on technology controlled by a strategic rival. Reliance's gigafactory at Jamnagar, the PLI scheme's 50 GWh targets, the entire edifice of India's clean energy manufacturing strategy: all of it rests on an assumption of continued Chinese cooperation that Beijing has no obligation to honour and every strategic incentive to withhold.

The episode, real or not, should concentrate minds.

Reliance's Accumulation Problem

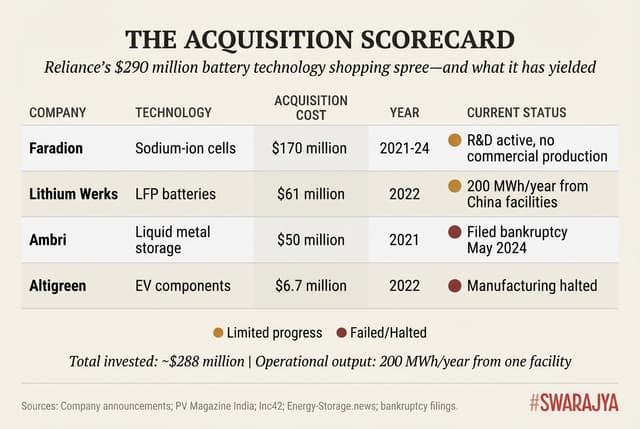

Reliance, to be fair, has not been idle. Since 2021, Reliance New Energy Solar has spent nearly $290 million acquiring battery technology companies spanning three distinct chemistries.

The crown jewel is Faradion, a UK-based sodium-ion pioneer acquired for approximately $170 million. Faradion holds over 29 patent families covering cell chemistry, architecture, and safety systems. In 2022, Reliance paid $61 million for the assets of Lithium Werks, bringing 219 patents for cobalt-free lithium iron phosphate technology and manufacturing facilities in China. It invested $50 million in Ambri, an MIT spinoff developing liquid-metal batteries for grid storage, and $6.7 million in Altigreen, an electric vehicle components firm.

The portfolio looks impressive on paper. In practice, results have been thin. Ambri filed for bankruptcy in May 2024 after Reliance declined bridge financing. Altigreen reportedly halted manufacturing the same year. Lithium Werks continues modest production of around 200 MWh annually from its Chinese facilities. Faradion's Sheffield headquarters conducts research, but commercialisation depends on the Jamnagar gigafactory—which is a year behind schedule and accumulating government penalties at ₹5 lakh per day under the PLI scheme.

The problem is not a shortage of acquisitions. It is a shortage of integration. Reliance has accumulated technology assets without building the indigenous research capacity to develop, adapt, and scale them independently. This is what makes even the possibility of Chinese technology denial so consequential: the acquired patents are not yet substitutes for proven manufacturing know-how.

The Jio Institute Anomaly

This makes one omission particularly striking. Reliance operates Jio Institute, a nascent university in Navi Mumbai that the company has committed ₹9,500 crore—over $1.1 billion—to building. The institution boasts serious leadership: Dr R.A. Mashelkar, former Director-General of the Council of Scientific and Industrial Research, serves as Chancellor; Dr Dipak Jain, former Dean of Kellogg and INSEAD, as Vice-Chancellor. Faculty have been recruited from Northwestern, Caltech, Toronto, and NTU Singapore.

Yet Jio Institute currently enrols only 180 students across three one-year postgraduate programmes: AI and Data Science, Management, and Sports Management. Research focuses on artificial intelligence applications through the Centre of AI for All. There is no engineering undergraduate programme. More puzzlingly, given Reliance's green energy commitment and its battery technology acquisitions, there is no dedicated research programme in battery chemistry, electrochemistry, or energy storage materials.

The disconnect is hard to explain. Reliance has spent $290 million buying battery patents from foreign companies while investing $1.1 billion in a university that conducts no battery research. It partners with IIT Bombay on BharatGPT, an indigenous AI model—a genuine deep-tech collaboration. It funds a Telecom Centre of Excellence at IIT Madras. But no equivalent partnership exists for the technology at the heart of its green energy ambitions.

One wonders whether the Hithium episode, whatever its precise contours, might prompt a rethink. The BharatGPT collaboration demonstrates that Reliance knows how to build serious academic-industry research partnerships when it chooses to. The question is whether battery technology will receive the same treatment—or whether the company will continue seeking technology transfer from abroad while its own institutional assets remain underleveraged.

What Government Has Done Right

To its credit, the Modi government has begun building the institutional architecture for exactly this kind of deep-technology investment. The Research, Development and Innovation Fund, announced in Budget 2025, represents Rs 1 lakh crore of "patient capital"—financing with 10-15 year horizons that traditional venture capital and banking cannot provide.

The fund's design addresses India's core innovation deficit. Roughly 36% of Indian R&D comes from business, far below the global norm of 65-70%. Corporate India devotes just 0.3% of GDP to in-house research—five times less than the world average. The ten largest non-financial firms, despite $43 billion in annual profits, spend under $1 billion on research collectively. The RDI Fund attempts to change this calculus by channelling public capital through professional fund managers who select private-sector projects, with a 50% co-investment requirement ensuring corporate commitment.

The structure is promising. Fifty-year, zero-interest loans to fund managers create genuinely patient capital. Exemptions from the General Financial Rules allow market-rate hiring and agile deployment. The focus on Technology Readiness Level 4 and above targets the "valley of death" where promising technologies perish between prototype and commercialisation. If executed with genuine autonomy—tolerating inevitable failures, insulating decisions from political pressure—the fund could catalyse exactly the deep-tech investment India needs.

This publication has covered the RDI scheme in detail elsewhere. The point here is simpler: the government has done its part. The question is whether India's corporate giants will do theirs.

The Missing Middle: Little Giants

Yet even the RDI Fund, significant as it is, addresses only one dimension of India's challenge. It targets large conglomerates and established institutions capable of absorbing Rs 50-100 crore investments. What about the smaller firms that form the backbone of any manufacturing ecosystem?

Here, China's "Little Giants" strategy offers a template India would do well to study. Beijing has cultivated over 14,000 little giants—small, privately owned enterprises operating in strategic industries from semiconductors to aerospace to battery materials. These are not conventional small businesses. They are highly specialised firms that have earned government recognition through rigorous assessment of technological capability. Ninety percent operate in manufacturing, with over 80% working in "strategic emerging industry chains."

The genius lies in structured competition. At the foundation are "innovative SMEs" identified at provincial level. The most promising ascend to "specialised SMEs," gaining support. Outstanding performers achieve national little-giant status. At the apex stand "manufacturing champions." Firms compete for recognition, incentives, and capital, with periodic reassessment ensuring only the capable retain their status. In 2022, 40% of IPOs on Shanghai, Shenzhen, and Beijing exchanges came from little giants.

India's MSME landscape could hardly be more different. Despite 63 million registered enterprises contributing 30% of GDP, 99% remain microenterprises with fewer than 20 workers. Regulatory frameworks inadvertently incentivise staying small: cross six employees and trade union laws apply; reach ten and the Factories Act kicks in; exceed 100 and retrenching workers requires government approval. MSME credit penetration stands at just 14%, compared with China's 37% and America's 50%.

India needs its own little-giants programme—a tiered recognition system that identifies technologically promising smaller firms, supports their ascent through financing and regulatory simplification, and integrates them into the value chains of larger corporations. The goal is to cultivate what Germans call the Mittelstand: specialised, globally competitive enterprises that dominate niche markets. Without this middle layer, India's battery ecosystem will remain a collection of giant assemblers dependent on foreign technology and tiny informal workshops producing nothing of strategic value.

From Vulnerability to Determination

The Reliance-Hithium episode—whatever actually transpired—has performed a useful service. It has surfaced a structural vulnerability that was always present but rarely discussed: India's clean energy transition depends on technology that China controls and could deny at will.

This is not cause for panic. It is cause for strategic clarity.

China built its technological sovereignty because the West kept saying no. BeiDou exists because America jammed GPS. Tiangong orbits because Congress banned NASA cooperation. Indigenous 7nm chips emerged because Washington blacklisted Huawei. In each case, denial bred determination, and determination bred capability.

India need not wait for its own "unforgettable humiliation." The near-miss—or the mere plausibility of one—should be sufficient to catalyse action. The policy architecture is taking shape: the RDI Fund provides patient capital; a little-giants programme could unlock the MSME ecosystem. What India needs now is for its corporate champions to match government ambition with their own.

Reliance has the resources. Its $27 billion cash reserves and $9.5 billion annual profits dwarf what China spent building BeiDou. Its acquired patents from Faradion and Lithium Werks provide a foundation. Its existing partnerships with IITs demonstrate capacity for deep academic collaboration. Whether indigenous development rather than technology transfer becomes the primary path is a choice the company will make in the coming months.

The question posed by the Hithium affair is not "did China say no?" It is "what will India do when China does?" The answer to that question will determine whether the country remains a technology taker or becomes, at last, a technology maker.

History suggests denial can be a gift—if met with determination rather than despair. India has been handed a warning. What it does with it is up to Reliance, and to India.

A public policy consultant and student of economics.